4th Qtr Review

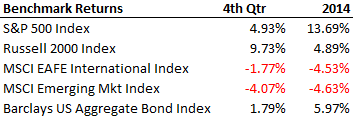

Since starting off the quarter marked by high levels of fear and falling stock markets, most U.S. markets rebounded and finished the year off strong. International and Emerging markets continued their weakness and finished the year in the red. Bonds bounced back from a negative 2013 to have a solid 2014. In this issue of Allgen’s quarterly market commentary we will discuss how the recent drop in oil prices affects the market, the potential for increased volatility in 2015 and the outlook for interest rates.

Since starting off the quarter marked by high levels of fear and falling stock markets, most U.S. markets rebounded and finished the year off strong. International and Emerging markets continued their weakness and finished the year in the red. Bonds bounced back from a negative 2013 to have a solid 2014. In this issue of Allgen’s quarterly market commentary we will discuss how the recent drop in oil prices affects the market, the potential for increased volatility in 2015 and the outlook for interest rates.

Recent Drop in Oil Prices

Oil recently dropping below $50 a barrel (see chart below) has prompted many people to ask how did that happen and what does it mean going forward. How it happened is simple: oil production has gone up at a faster rate than oil demand. Because of recent technology enhancements and shale discoveries in the U.S. oil industry, production as increased about 60% in the last 5 years from 5.5 million barrels per day to almost 9 million barrels per day. The increase in production in the U.S. has meant that we import far less oil from other countries. In fact, the U.S. no  longer imports oil from Nigeria. That means all the oil that the U.S. was importing is now additional supply for the rest of the world thereby causing a supply glut. At the same time, world oil consumption/demand has slowed down significantly. What does this mean going forward? Although there are positives and negatives with oil prices this low, we believe it is overall a net positive. Cheaper oil prices are good for consumers and leave more money available to spend each month. This would have a positive effect on sectors of the economy that benefit from lower oil prices like transportation, retail and industrial. Historically positive economic surprises have been correlated to lower oil prices. From a global perspective countries that derive the majority of their GDP from consumption outweigh by a 2/3 margin countries that derive a large portion of their GDP from oil exports. The negatives from cheap oil would be that certain regions of America where oil shale makes up a large portion of the local economy could see miniature recessions, confined to those local areas. Also countries that are large exporters that are forced to cut social programs because of larger deficits may see some social unrest. We believe in the end market forces will take over and countries and companies will be forced to cut production which should eventually bring supply and demand back to an equilibrium.

longer imports oil from Nigeria. That means all the oil that the U.S. was importing is now additional supply for the rest of the world thereby causing a supply glut. At the same time, world oil consumption/demand has slowed down significantly. What does this mean going forward? Although there are positives and negatives with oil prices this low, we believe it is overall a net positive. Cheaper oil prices are good for consumers and leave more money available to spend each month. This would have a positive effect on sectors of the economy that benefit from lower oil prices like transportation, retail and industrial. Historically positive economic surprises have been correlated to lower oil prices. From a global perspective countries that derive the majority of their GDP from consumption outweigh by a 2/3 margin countries that derive a large portion of their GDP from oil exports. The negatives from cheap oil would be that certain regions of America where oil shale makes up a large portion of the local economy could see miniature recessions, confined to those local areas. Also countries that are large exporters that are forced to cut social programs because of larger deficits may see some social unrest. We believe in the end market forces will take over and countries and companies will be forced to cut production which should eventually bring supply and demand back to an equilibrium.

Potential for Increased Volatility in 2015

Since 2013 U.S. stock markets have seen little volatility. In fact, for the 2 years prior to October 2014 the stock market had not seen a pullback in stocks greater than 6%. Since October that trend started to  change where we are now seeing increased volatility. As you can see (chart on left) the volatility indicator (VIX) which measures volatility in the market has been decreasing since 2008 until recently where the long-term downtrend was broken to the upside. We believe the increase in volatility is partly due to the fact the Federal Reserve is no longer stimulating the economy thru its bond buying program called quantitative easing (QE). At the same time the bull market that started 5 years ago may be starting to mature. What does this mean for investors? Stock markets may continue to have wild swings in both directions this year and that could cause investors to have higher levels of fear. We do still believe that the long-term secular bull is intact, but the market could have a significant correction at some point this year. As we pointed out in our last commentary fear isn’t necessarily a bad thing. In fact, when markets took a drop in October we were able to sell some bonds as they went up and buy some stocks as they went down. High levels of fear are almost always associated with market bottoms. We see volatility as an opportunity to take advantage of pricing anomalies which allow us to buy good companies at temporarily lower prices. It’s important to keep a long-term mind-set when investing and try not to allow the emotions of a temporary setback in the stock market affect your overall investment strategy.

change where we are now seeing increased volatility. As you can see (chart on left) the volatility indicator (VIX) which measures volatility in the market has been decreasing since 2008 until recently where the long-term downtrend was broken to the upside. We believe the increase in volatility is partly due to the fact the Federal Reserve is no longer stimulating the economy thru its bond buying program called quantitative easing (QE). At the same time the bull market that started 5 years ago may be starting to mature. What does this mean for investors? Stock markets may continue to have wild swings in both directions this year and that could cause investors to have higher levels of fear. We do still believe that the long-term secular bull is intact, but the market could have a significant correction at some point this year. As we pointed out in our last commentary fear isn’t necessarily a bad thing. In fact, when markets took a drop in October we were able to sell some bonds as they went up and buy some stocks as they went down. High levels of fear are almost always associated with market bottoms. We see volatility as an opportunity to take advantage of pricing anomalies which allow us to buy good companies at temporarily lower prices. It’s important to keep a long-term mind-set when investing and try not to allow the emotions of a temporary setback in the stock market affect your overall investment strategy.

2015 Outlook on Interest Rates and Bond Update

Most economists believe that the Fed rate hike is inevitable this year. One indicator for future rate hikes is seen by monitoring the interest rate futures. According to CME Group FedWatch there is a 70% probability that interest rates will go up in 2015 and have the highest probability to end the year between 0.5% and 0.75%. Currently the Fed Funds Rate is at 0% – 0.25%. Consensus points to the Fed starting to gradually increase rates in July of 2015, but if global economic growth decreases the Fed may take a longer time before they raise rates. Long-term, Allgen maintains that we are coming out of a balance sheet recession (too much debt followed by deleveraging) which is historically associated with gradually increasing rates. At this point we don’t see a major threat of rates increasing rapidly.

Bonds have 3 main uses in a portfolio: increasing stability (lowering volatility), providing a stream of income, and increasing liquidity. Of those three, the most important thing they have done since 2007 for our clients was provide security when markets pulled back; they’ve allowed us to rebalance portfolios and sell some bonds as they have gone up and buy some stocks as they have come down (and vice versa).

Going Forward

While the recent, sharp drop in oil prices has caused some alarm in the market, we believe cheaper oil is a net positive. Markets have also shown an increase in volatility which is likely to continue in 2015. While increases in volatility usually goes along with increased fear among investors, history has shown that times of heightened fear have been good times to buy. Moreover, periods when markets take wild swings up and down have favored our management style as we take a more proactive approach to strategically rebalancing portfolios, while attempting to take advantage of pricing anomalies. We encourage our clients to keep a long-term investment perspective in mind and try to avoid the temptation to allow short-term market movements to drive you to make emotionally based decisions regarding your investments. While stocks provide long-term growth potential, bonds have served their role in protecting capital, reducing volatility and providing income. Probability does favor an increase in rates this year but we think that the increases, once they begin, will be gradual. We continue to manage risk first in all of our investments, while seeking to outpace our clients’ appropriate benchmark over the long-term net of our fees.

Written by:

Jason Martin, CFP®, CMT, Chief Investment Officer Allgen Financial Services, Inc.;

Paul Roldan, Chief Executive Officer; Chris Damiano, Operation Specialist